Becoming a homeowner is both exciting and overwhelming, isn’t it? There are new responsibilities around every corner, and one of the most important is making sure your insurance truly safeguards your investment. But how do you know if your policy does what you think it does? Are you confident you’re protected against life’s curveballs, or do you worry there are hidden gaps?

We get it. Many new homeowners feel anxious about insurance. We’re here to help you understand what to look for, what questions to ask, and how to make confident choices for your family’s future. Ready to dig in and feel more at ease about your coverage?

New Homeowner? Let’s Make Sure Your Policy Matches Your Needs

You’ve taken the leap into homeownership—now it’s time to make sure your insurance truly protects your investment. At Chapman Insurance Group, we help new homeowners like you feel confident in their coverage, so you’re not left guessing when life throws the unexpected your way.

Why choose us? Our local team understands Florida’s risks, from rising construction costs to storm damage exclusions. With access to over 35 carriers and transparent advice, we help you avoid gaps, lock in fair pricing, and ensure your home is covered from all angles.

Ready to review your homeowners policy with an expert? Contact us today for a personalized insurance checkup designed around your life, your home, and your future.

Key Takeaways

- A thorough policy review ensures your homeowners insurance aligns with your home’s rebuild cost and current needs.

- Regularly check your coverage areas, including dwelling, personal property, liability, and additional living expenses, to avoid common gaps.

- Standard homeowners policies typically exclude flood, earthquake, and water backup damage, so consider separate policies if you’re in high-risk areas.

- Evaluate and compare insurance policies based on coverage fit, deductibles, financial strength, discounts, and real customer reviews.

- Update your policy after major life or home changes and conduct annual reviews to keep your protection up to date.

- Consulting with an insurance professional can help you address concerns and make confident choices regarding your homeowners insurance policy review.

Understanding Homeowners Insurance Policies

Homeowners insurance might sound straightforward, but when you look closely, there’s a lot to unpack. The basics cover your house’s structure and your personal belongings if there’s a fire, theft, or other covered events. But the protection doesn’t stop there. Most policies also cover liability if someone gets hurt on your property and may include living expenses if your home becomes uninhabitable after an insured event.

There are different policy forms, with HO-3 being the most common for single-family homes. Each form sets out what’s covered, and, equally important, what’s not. Understanding this framework can help you spot whether your policy is a good fit or if you might need extra protection.

Are you clear on which type of policy you currently have? If not, it’s worth asking your agent for a quick rundown.

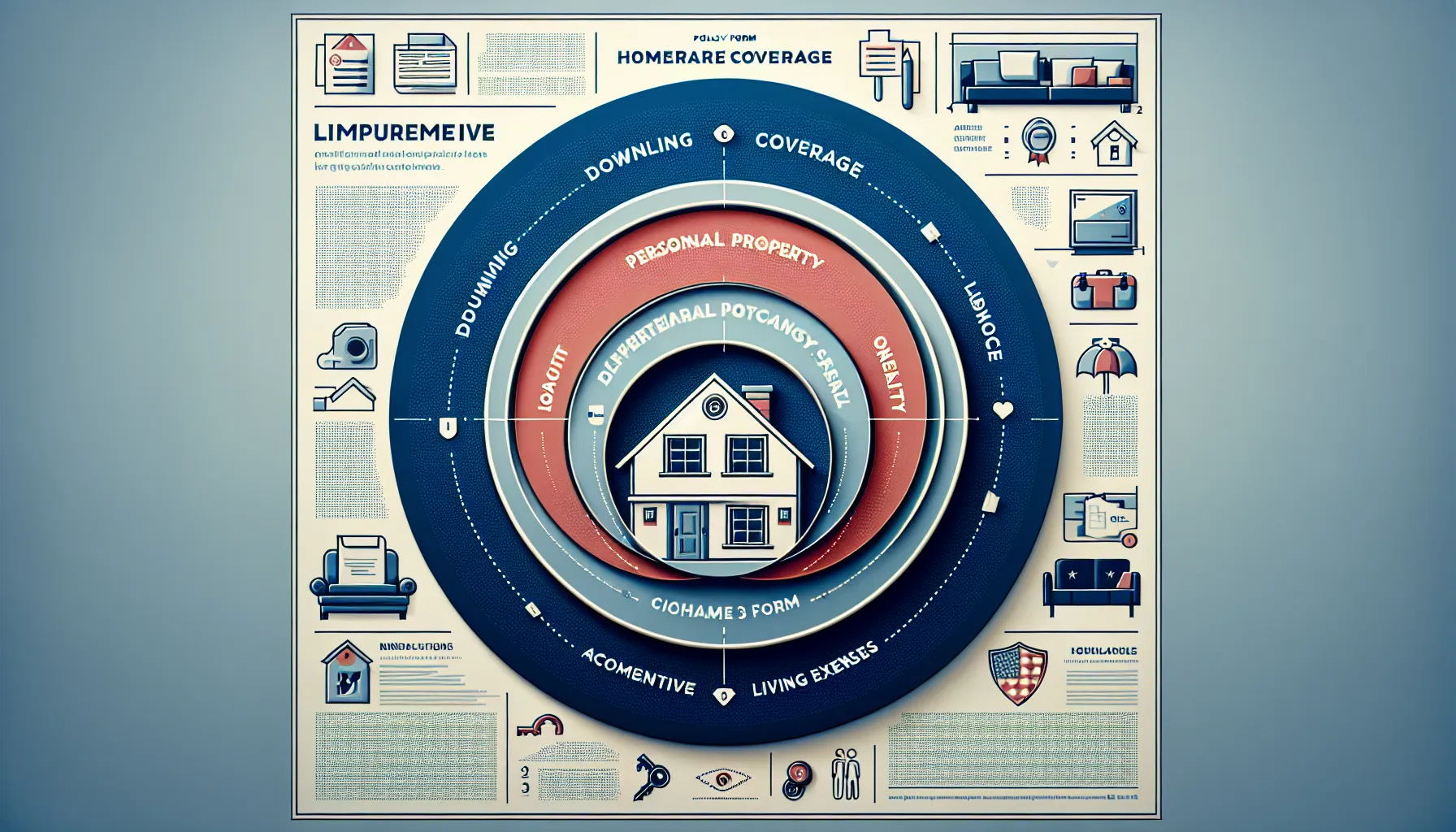

Key Coverage Areas to Examine

Let’s break down the critical areas you should pay attention to when reviewing your insurance documents:

Dwelling Coverage

This covers the main structure of your home. Double-check that the amount matches your home’s rebuild cost, not just its market value. Construction prices can rise, so update this amount if you’ve done renovations or if it’s been a while since your last review.

Personal Property

From your furniture to electronics, personal property coverage helps you replace valuables after loss or damage. Make a rough inventory and compare it against your limits. If you own high-value items, consider adding coverage for those specifically.

Liability Protection

If a guest slips and falls or if your pet causes an accident, liability coverage protects you financially. It’s easy to underestimate your exposure here. We often recommend higher limits for peace of mind, don’t be shy about asking if boosting your coverage might make sense.

Additional Living Expenses (ALE)

What if a fire means you can’t stay at home during repairs? ALE covers hotel costs, meals, and other expenses. Review the dollar limit and time frame attached to this section to avoid unpleasant surprises.

Are there any areas where you’re uncertain or feel your coverage might fall short? Jot them down, these are exactly the topics you’ll want to discuss during a policy review.

Common Gaps and Exclusions in Policies

Insurance can’t cover everything, and every policy includes exclusions and limits. Here are a few often-missed gaps:

- Flood and Earthquake Damage: Standard homeowners insurance rarely covers these perils. If you’re in a high-risk zone, standalone policies may be necessary.

- Water Backup: Damage from sump pump failures or sewer backups is common, and commonly excluded. Carefully check, and ask about endorsements that can add this protection.

- Mold, Wear and Tear: Most policies won’t cover damage from neglect, gradual deterioration, or mold due to preventable conditions.

- Expensive Valuables: Jewelry, fine art, and collectibles typically have low sub-limits. Scheduling these items separately can protect your investments.

Have you spotted any of these exclusions in your policy? Would a conversation with an insurance professional help you gain more clarity about what’s not protected?

How to Evaluate and Compare Policies

Shopping for insurance doesn’t have to feel stressful. Here’s how we recommend evaluating and comparing your options:

- Match Coverage to Your Needs: Don’t focus just on price. Make a list of your must-haves and nice-to-haves, then see which companies offer the coverage that aligns with your situation.

- Look at Deductibles: The deductible is what you pay first before insurance kicks in. Lower deductibles mean you’ll pay less out of pocket in a claim, but often cost more each month.

- Review Financial Strength: You want a company that will be there when you need them most. Check independent ratings to confirm reliability.

- Ask About Discounts: Many insurers reward things like security systems, bundling policies, and claims-free histories.

- Read Client Reviews: Feedback from real people (like the ones you’ve seen above) offers clues to the service experience you can expect.

Do you already have coverage in place, or are you weighing quotes from multiple providers? It may help to write down your priorities before reaching out.

Steps to Update or Change Your Coverage

There are times you’ll need to update (or even change) your policy entirely:

- Major Home Upgrades: Renovations can increase rebuild costs and mean you need higher dwelling coverage.

- Life Changes: Moving in with a partner, welcoming children, or starting a home business can all affect your insurance needs.

- Finding a Better Price or Fit: Sometimes, you may discover your current insurer isn’t offering the flexibility or value you want.

Here’s how to go about making a change:

- Review and List Your Needs: Start with what’s changed and what you need the new or updated policy to cover.

- Talk with Your Agent: A conversation with a real person is invaluable. Ask questions, share concerns, an agent can help tailor the policy to fit your life.

- Compare Before You Switch: Never cancel your old policy before your new one is in effect. This avoids any accidental gaps in coverage.

- Complete the Paperwork: Once you’ve chosen, sign any needed documents and keep copies for your records.

Have you experienced a big life change or completed a renovation recently? It could be time to give your coverage a fresh look.

Tips for Ongoing Policy Reviews

We believe insurance shouldn’t be “set it and forget it.” Regular reviews are key to staying protected as life moves forward. Here’s how to approach reviews:

- Mark Your Calendar Annually: A yearly check-in is a great practice. Set a reminder or use your renewal date as a prompt.

- Keep Notes on Changes: Any home improvements, purchases of expensive items, or changes in your household should trigger an insurance conversation.

- Ask About New Products: The insurance landscape is always shifting. New products or discounts may be available that suit you better now than when you first signed up.

- Review Your Deductibles and Limits: Make sure both still fit your financial goals and comfort level.

- Stay Informed of Local Risks: If your neighborhood risk profile changes, like new flood zone maps or wildfire activity, bring it up at your review.

Do you already have an annual insurance review on your calendar? If you don’t, is now the time to start that habit?

Conclusion

Owning a home comes with many responsibilities, but staying proactive with your insurance doesn’t have to be overwhelming. By understanding your policy, keeping an eye out for gaps, and checking your coverage each year, you can rest easy knowing you’re doing your best to protect what matters most.

If you ever feel stuck or uncertain, reaching out to a professional who listens and understands your concerns can make all the difference. After all, peace of mind is priceless. So, when was the last time you reviewed your policy, and are you ready to make sure your home and family are truly protected?

Frequently Asked Questions for New Homeowners’ Policy Review

What should new homeowners look for during a policy review?

New homeowners should examine their insurance policy’s dwelling coverage, personal property protection, liability limits, and additional living expenses coverage. Evaluating exclusions, such as for floods or valuable items, is crucial to ensure complete protection and avoid unexpected gaps.

How often should I review my homeowners insurance policy?

Experts recommend reviewing your homeowners insurance policy at least once a year or after significant life changes, such as renovations, major purchases, or changes in household composition, to ensure your coverage still matches your needs.

Does standard homeowners insurance cover flood or earthquake damage?

No, standard homeowners insurance policies typically exclude flood and earthquake damage. If you live in an area prone to these hazards, you should consider purchasing separate flood or earthquake insurance policies for adequate protection.

What are common gaps in homeowners insurance policies?

Common gaps in homeowners insurance include lack of coverage for water backup, mold, certain valuable items like jewelry or art, and neglect-related damage. Reviewing exclusions and discussing endorsements with your agent can help close these gaps.

How do I compare homeowners insurance policies for the best fit?

Compare homeowners insurance policies by matching coverage to your needs, reviewing deductibles, checking the insurer’s financial strength, asking about discounts, and reading customer reviews to assess service quality before making a decision.

Can I increase my liability protection with my current homeowners policy?

Yes, most insurers allow you to increase your liability coverage limits for added peace of mind. Discuss your needs and potential risks with your insurance agent to determine the appropriate level of protection for your situation.